The Gulf Cooperation Council (GCC) unites six Arab powerhouses—Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the UAE—to boost political and economic collaboration. Known for their vast wealth and boundless opportunities, these nations are set to become the next epicentre of global apparel dominance. This lucrative market offers a golden opportunity for the Indian apparel industry to forge solid partnerships with the GCC, which is India’s largest trading bloc. In FY 2022–23, trade with the GCC accounted for 15.8 per cent of India’s total trade, surpassing the 11.6 per cent share with the European Union.

Excitingly, India and the GCC have resumed talks to finalise a free trade agreement, promising new business opportunities for both sides. India has already signed a Comprehensive Economic Partnership Agreement (CEPA) with the UAE, significantly boosting trade. Bilateral trade has grown from US $ 72.9 billion to US $ 84.5 billion, marking a year-on-year increase of 16 per cent.

Economic landscape and apparel market projections

A recent report by the Boston Consulting Group (BCG) predicts that the financial wealth of GCC will grow steadily, with a Compound Annual Growth Rate (CAGR) of 4.7 per cent

from US $ 2.8 trillion to US $ 3.5 trillion between 2022 and 2027.

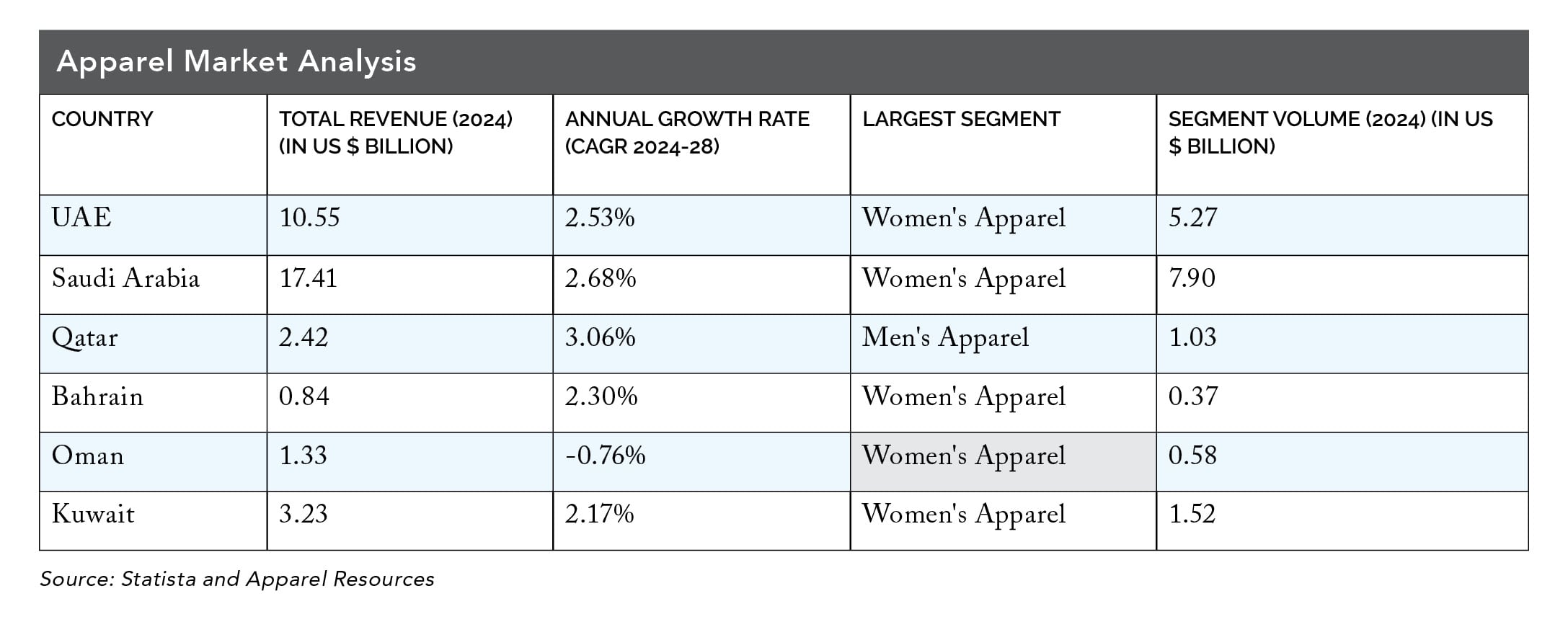

As per Statista, the apparel market in the GCC is expected to reach a total revenue of US $ 35.78 billion by 2024. This market is estimated to grow by 2.48 per cent annually from 2024 to 2028. The largest segment within this market is Women’s Apparel, which is projected to have a market volume of US $ 16.67 billion in 2024. On an average, each person is expected to purchase 43.8 pieces of apparel in 2024. By 2024, about 96 per cent of sales in the apparel market will be from non-luxury items. There is also a growing demand for modest fashion styles in GCC countries.

Markedly, the collective apparel import of GCC stood approximately at US $ 10 billion in 2023, 20 per cent of which (~ US $ 2 billion) came from India.

Consumer spending capacity makes GCC a desirable market

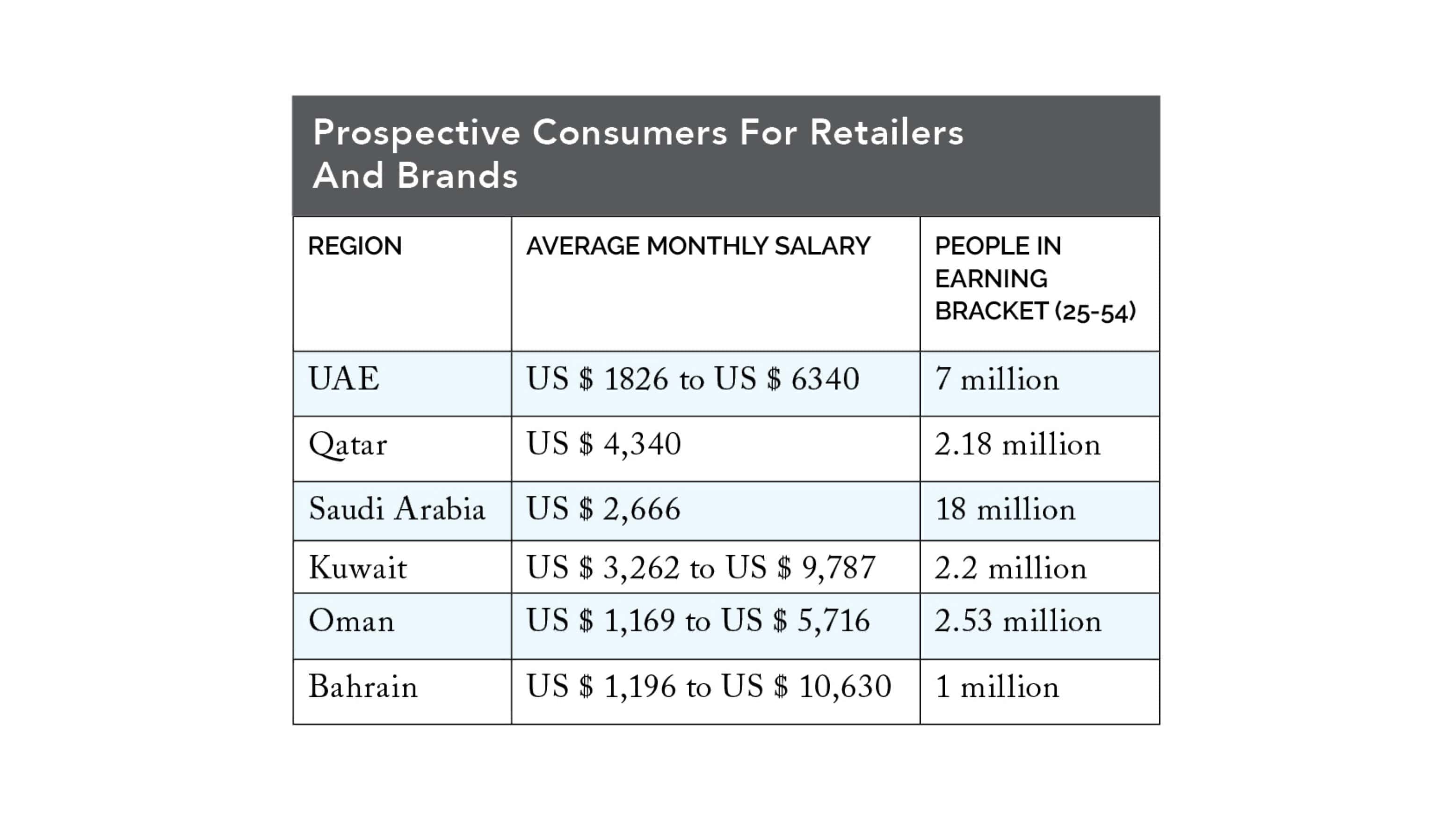

The GCC region boasts some of the highest per capita incomes globally, with consumers willing to spend significantly on fashion and lifestyle products. Having around 40 million people with taxable average monthly salary between US $ 2,000 – US $ 6,500 is comparable to any of the internal group of countries. In relation to the total population, per-person revenue (in apparel) of US $ 592.70 is expected in 2024 in GCC. This signifies the huge buying power of the consumers for the local retailers and brands.

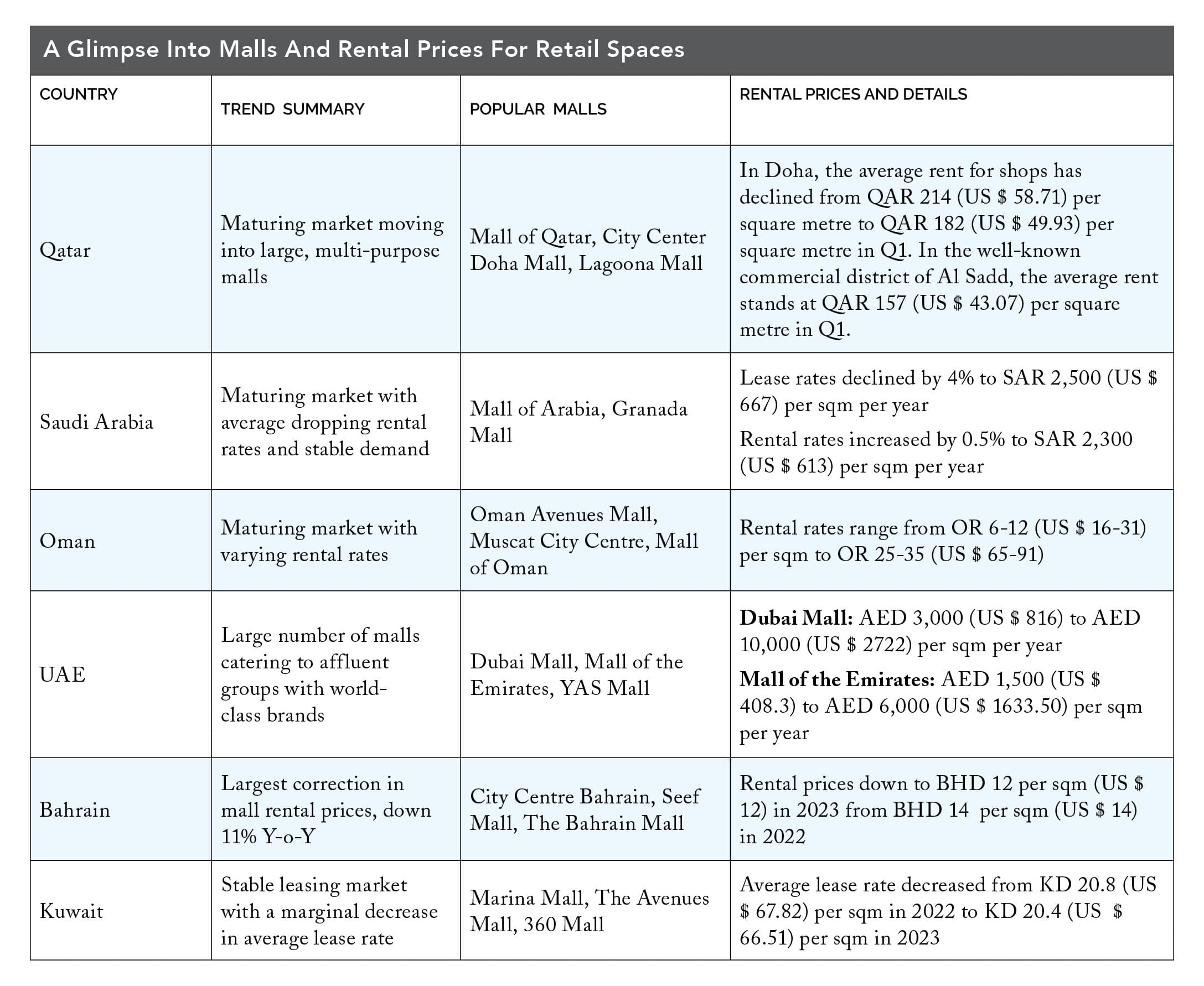

Retail space is poised to grow – thanks to increase in buying

Retail space is poised to grow – thanks to increase in buying

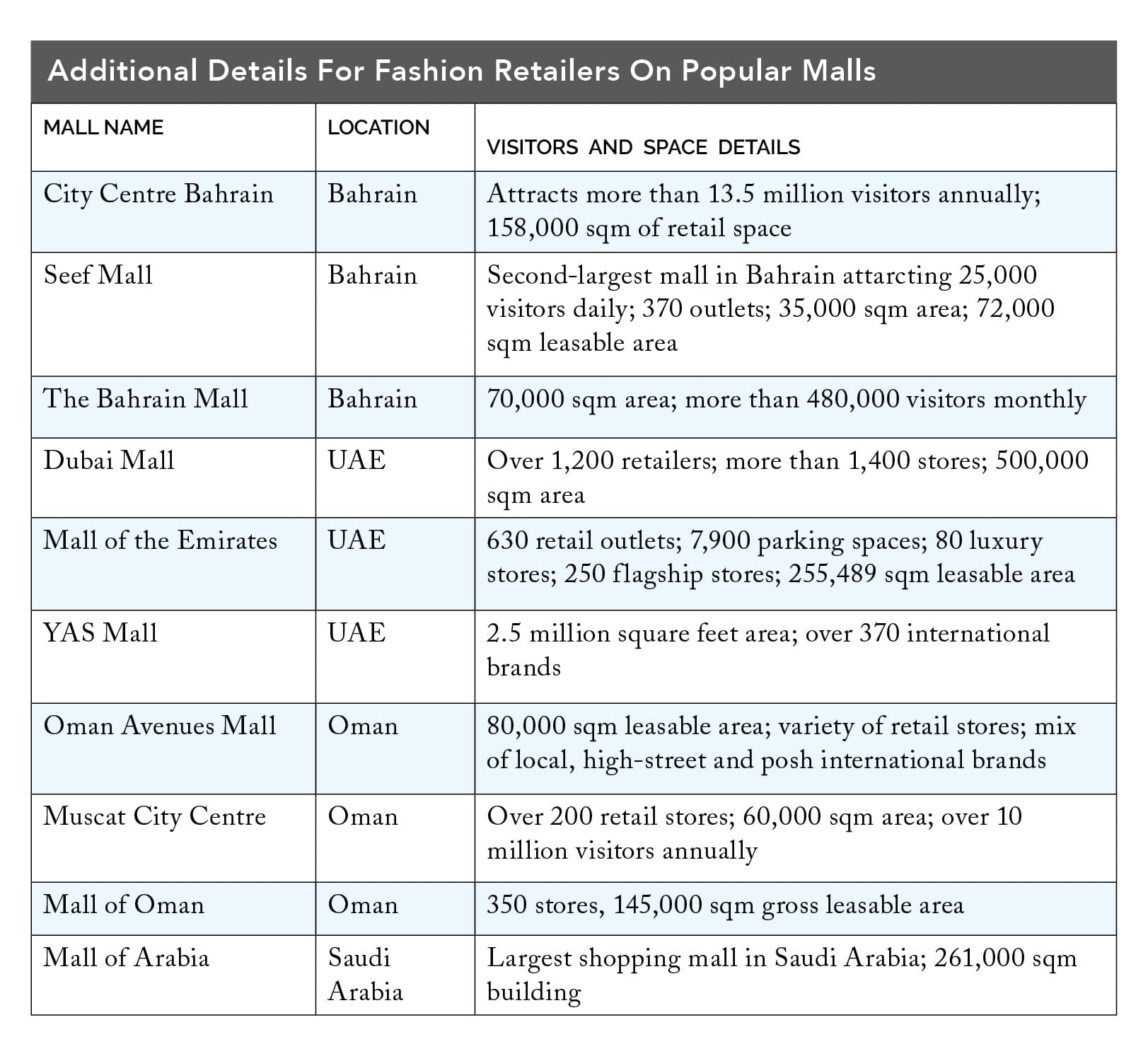

When it comes to GCC, there’s no dearth of stores catering to all kinds of fashion tastes! With 80 per cent completion of projected additions to the retail space, 4.5 million sqm of retail space is likely to come up in the GCC until 2026, taking the total organised retail Gross Leasable Area (GLA) in the region to 23 million sqm. Whereas organised retail GLA is anticipated to grow at a CAGR of 4.5 per cent during the period.

Exploring fashion retailers

Al Futtaim Retail, based in the UAE, is a significant conglomerate with over 44,000 employees, engaged in various ventures. Notable acquisitions include franchise rights to Marks and Spencer locations in Hong Kong and Macau and brands from global fashion giant Inditex (Zara, Massimo Dutti, Pull&Bear, Bershka, Oysho, Zara Home), as well as other fashion brands like Ted Baker, Lacoste, Sandro and others.

Majid Al Futtaim, also based in the UAE, operates hypermarkets, supermarkets and fashion specialty stores. Its fashion portfolio includes Abercrombie & Fitch, Hollister, AllSaints and Lululemon Athletica.

Landmark Group, headquartered in Dubai, is a multinational conglomerate with over 55,000 employees and 2,200 outlets across 21 countries. The group provides a value-driven product range for the entire family through a diverse portfolio of 57 brands – constituting 27 own brands and 30 franchise brands. The brands under Landmark that have fashion as a category include Centrepoint (a destination bringing together the Group’s four core retail brands), Babyshop (one-stop destination for kids between 0-16 years), Splash (multi-brand fashion retailer), Lifestyle (home décor, fashion accessories, beauty products, gifts and much more), Shoe Mart (multi-brand footwear and accessories store), Max (value fashion and footwear store), Iconic (fashion, art, makeup and gadgets), Sports One (multi-brand, multi-category sporting goods retailer), Shoexpress (value footwear and accessories store), Landmark International (a division that includes international franchise brands – New Look, Koton, Reiss, Lipsy and Yours) and Shoe Mart International Footwear Division (a division that includes franchise footwear brands – Kurt Geiger, Ecco, Pablosky, Dumond, Nose, Steve Madden, BLOCCO 31, Aerosoles and Carpisa). Made for young, mobile and tech-savvy customers across the GCC, STYLI is an e-commerce platform under the Landmark Group for fashion.

Apparel Group LLC, another major UAE-based conglomerate, operates over 2,200 retail stores in 14 countries, predominantly in the GCC. Its brands include Victoria’s Secret, Charles & Keith, Aldo, Bath & Body Works and others.

LuLu Group International, headquartered in Abu Dhabi, operates hypermarkets and retail outlets across Asia and the Middle East. LuLu Hypermarket offers fashion brands such as Longchamp, Guess, Lacoste and Fila. Chalhoub Group, based in Dubai, operates over 650 stores across eight countries, featuring luxury brands like Louis Vuitton and Dior and retail franchises like Saks Fifth Avenue. Al Tayer Group, also from Dubai, operates nearly 200 stores across six Middle Eastern countries, focusing on luxury brands.

AZADEA Group, a major lifestyle retailer, manages over 700 stores across 14 countries, covering sectors from fashion to multimedia. Alshaya Group from Kuwait manages nearly 70 retail brands, including Mothercare and Victoria’s Secret, across multiple regions. Namshi – part of the Noon Group – is the Middle East’s largest online fashion shopping hub for women, men and kids. Since 2011, it has grown to offer an extensive selection of leading brands as well as its own private labels. Al Nasser, also from Kuwait, focuses on sports and high-street fashion with a strong presence in several countries.

These retailers represent a diverse landscape of fashion and retail in the GCC, catering to various consumer needs across the region.

Decoding Gulf fashion

Middle Eastern consumers are experienced and increasingly savvy. For instance, young Saudis are embracing streetwear, creating a thriving fashion subculture in the Kingdom that blends contemporary fashion with traditional influences with brands like 1886 and Not Boring being amongst the top streetwear brands catering to Saudi Arabia’s young population. For current streetwear trends, there is a notable interest in oversized silhouettes; bold, vibrant colours; retro-inspired designs; and sustainable fashion. Mixing high-end designer pieces with streetwear elements is also a popular trend. A second trend in Saudi Arabia seems to be a fusion between traditionalwear and modern fashion sensibilities. Saudi fashion is about embracing traditional culture with its vision of modern elegance.

Similarly, in Qatar too, the traditional abaya, once a symbol of modesty, has transformed into a fusion of heritage and modern influences. Western fashion elements, such as tailored cuts, contemporary silhouettes and innovative fabrics, have found their way into the traditional Qatari abaya, creating a unique blend of tradition and modernity.

Modest fashion is on the rise as a trendy choice. It’s about stylishly covering up, featuring long dresses, maxi skirts and hijabs. Bright hues such as orange, pink and blue are in vogue, appearing in both traditional attire and contemporary fashion. Bold prints and patterns also make a statement.

In the UAE, one of the hottest trends right now is desert-inspired couture. Sustainable fashion has made its mark in the city’s fashion landscape. From eco-friendly fabrics to upcycled designs, Dubai’s fashion-forward women are making conscious choices.

A key growth tailwind in the Gulf consumer sector is the exponential increase in e-commerce adoption. Incumbent retailers are competing with a growing number of digital market entrants, including super apps, social media players, aggregators and global e-marketplaces. The UAE retail mobile-commerce market is projected to grow at 19 per cent CAGR between 2020 and 2025. The outlook for UAE’s overall e-commerce retail market is equally strong, with expectations that it could reach US $ 8 billion by 2025.

Opportunities for Indian apparel brands

GCC region presents a thriving and lucrative opportunity for Indian apparel brands and retailers that have already started foraying in the Middle East to expand their retail presence. With its burgeoning economy, increasing disposable income and a strong appetite for fashion, the GCC market offers Indian apparel brands a fertile ground for growth and expansion. Being Human, Campus Sutra, Shree amongst others have already opened their stores in the Middle East region.

According to Anuj Kejriwal, CEO and MD, ANAROCK Retail, Saudi Arabia and UAE continue to lead the retail sales regionally, cumulatively accounting for 79 per cent – 80 per cent of the total sales by 2026. He says that modern-age apparel brands like FableStreet, The Souled Store and Suta would be well-placed to position themselves in the malls of the region. ANAROCK Retail is a leading real estate company in India and has a presence in the GCC as well through ANAROCK Middle East, a subsidiary of the ANAROCK Group, a real estate firm in Dubai’s luxury market.

According to Sandip Hazra, Director, PwC, GCC also offers great opportunities for Indian designers. “This year, designer Manish Malhotra opened a 5,000 sq.ft. store in the Dubai Mall, one of the world’s most sought-after destinations for luxury brands. It is the first South Asian store to have a space in the mall’s Fashion Avenue, a section dedicated to international luxury brands. Dubai has 27 per cent Indians and 12 per cent Pakistanis representing a significant market.” Indian designers like Sabyasachi, Anita Dongre and others

are already popular in the GCC market.

GCC countries have been making concerted efforts to diversify their economies and attract foreign investments. This includes offering incentives, reducing trade barriers and creating favourable regulatory frameworks, all of which can benefit Indian apparel brands looking to establish a foothold in the region.

Some of the notable wholesale apparel importers of the Gulf region include RNA Resources Group Ltd., and BMA International Fze from the UAE; Nabil Mohsen Saleh Al Rashedi Trade and Gulf Garments Trading Co. Ltd., from Saudi Arabia; Azaiba Clothing Factory and Oman Textile Holding Company SAOG from Oman.